At various intervention levels, the housing deficit in Nigeria has seen different approaches to tackling it with little or no results. But experts have offered fresh insights into how targeted and low-cost financing can resolve the seemingly intractable problem.

It is expected that targeted funding initiatives will ameliorate incremental construction or self-funded construction problems. This would ease pressure on the public sector, leaving room for governments to address appropriate town planning, building standards, the provision of land title issues, and infrastructure trunk-lines for water and power.

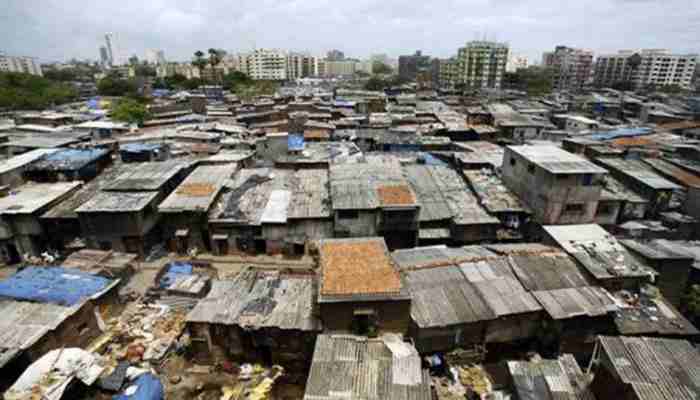

Though Babatunde Fashola, Nigeria’s works and housing minister, says Nigeria does not have a housing deficit, dismissing whatever the country has as an urban problem, housing shortage in the country is real and many sector stakeholders are in agreement with this.

The deficit is estimated variously at 17 million, 20 million and 22 million units, depending on who one is speaking to.

According to Danladi Matawal, former director-general/CEO, Nigerian Building and Roads Research Institute (NBRRI), the deficit is even more than the stated figure, citing findings by Worldometer (2017), which noted that from 2012 to 2018, Nigeria’s population increased from 168,240,403 to 191,835,936, showing a significant addition of 23,595,533 people to the population.

“The housing deficiency has, therefore, climbed and is likely to worsen in the nearest future if urgent steps are not taken by the government in conjunction with all stakeholders to address the problem,” he said at an international housing conference in Abuja.

This explains why, as efforts intensify to return the country to the path of sustained growth, there has been an increased focus on the real estate sector—specifically the affordable housing market. The persisting and widening deficit has seen more and more people unable to afford the cost of owning their own home.

Besides investment in affordable housing, there are also schemes such as buy-to-let, and affordable mortgage schemes including the national housing fund (NHF) and lately the Nigerian Mortgage Refinance Company (NMRC) which offer low interest rates.

The experts added that efforts at tackling the deficit resulted in the formation of the Real Estate Developers Association of Nigeria (REDAN), the Building Materials and Manufacturers and Producers Association of Nigeria (BUMPAN).

At the continental level, organisations like Shelter Afrique offer a much-needed injection of large-scale private funding to address both demand-side and supply-side constraints. As the only pan-African financial institution dedicated solely to the growth of Africa’s housing and real estate sector, Shelter Afrique offers developers a payment structure similar to those available in Germany, the United Kingdom and Hungary.

These offer favourable terms like 10-year loan payment periods at competitive interest rates. Indeed, the pan-African housing finance institution has a clear mission – to increase access to quality, low-cost housing across Africa.

“Shelter Afrique offers a range of financing facilities to support the delivery of affordable housing and to stimulate the demand side across Africa including but not limited to Lines of Credit and Project Finance,” according to Andrew Chimphondah, GMD/ CEO, Shelter Afrique.

Besides a $619 million commitment to the Solar Homes Systems Project, to install solar home systems for up to 5 million households, serving about 25 million individual Nigerians who are not currently connected to the national grid, Chimphondah disclosed plans by the organization to support affordable housing in Nigeria.

“Shelter Afrique is committed to supporting large scale, affordable housing schemes in Nigeria through the issuance of a N250 billion bond. This is planned to provide affordable housing and homeownership to low and medium income home buyers, consequently improving their standard of living,” he assured.

Recently, the pan-African housing finance organization partnered REDAN to finance 12,000 affordable housing units in Nigeria. The memorandum of understanding, signed in July 2021 will see 6,000 units developed across the six geopolitical zones of Nigeria in the first phase of the project.

However, for international agencies such as Shelter Afrique, making inroads into new territories like Nigeria can be difficult. Exchange rate volatility and sky-high interest rates make financing projects a dicey game, but there are ways to mitigate the issue.

While Shelter Afrique, alongside other institutions like the African Development Bank (AfDB), is working hard to address the staggering housing deficit across the continent, domestic parastatals and organisations also play a crucial role.

In Nigeria, the Federal Mortgage Bank of Nigeria (FMBN) has been consistent and proactive in providing loans and financing across the real estate value chain. In 2020 alone, FMBN distributed $30.5 billion (US$74 million) through its service offerings to bring home ownership within the reach of more citizens.

source: businessday ng